The following breakout is a summary of GSUSA’s financials from FY2020, and this data comes from three sets of reports:

Before delving into the data, you may want to read through this article called How to Navigate Council Finances if you aren’t already familiar with nonprofit financial documents and reports. Even though it’s specific to councils, it explains what some of the following information provides, what it means, and its context.

“FY2020” covers the period between 10/1/2019 and 9/30/2020.

Note that this is NOT an in-depth review of finances, and conclusions should not be based on this very brief snapshot. For a more complete picture, one should look through all balance sheets and review them over a number of years.

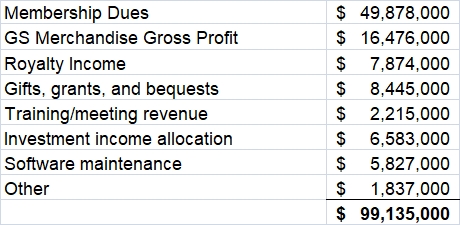

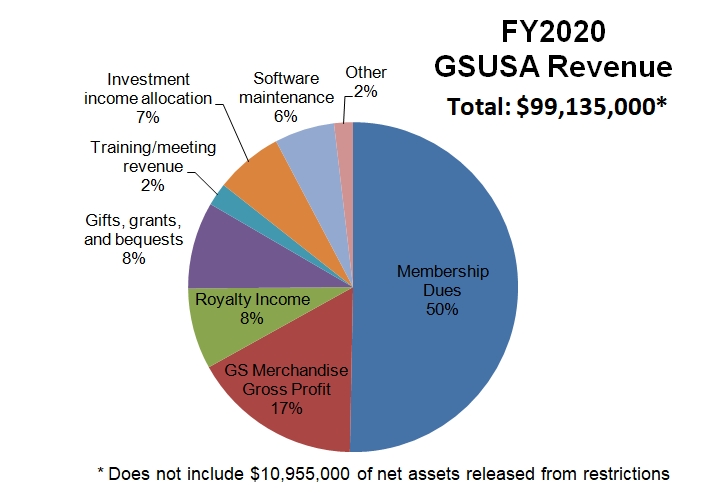

REVENUE

These figures come from the FY2020 audit (pg. 6):

Software maintenance consists of payments from councils for the licensing use of Volunteer Systems 2.0, the GSUSA IT platform that all councils are required to use.

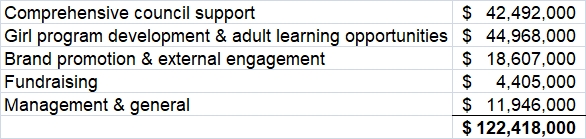

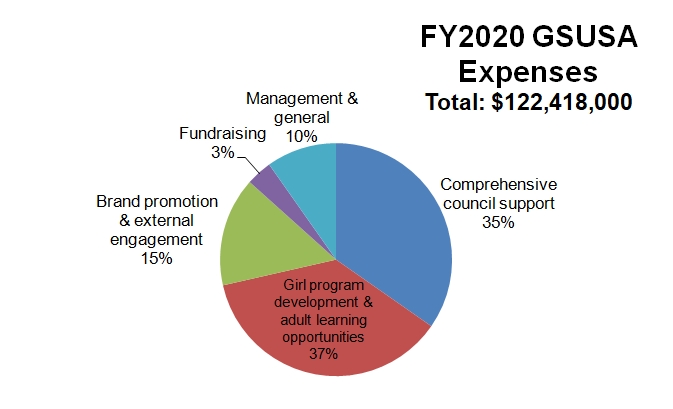

EXPENSES

Expenses for FY2020 were as follows in these major categories (FY2020 audit, pg. 6):

Expense category definitions are found on pg. 10-11 of the audit. Many things can fall under “Comprehensive council support” and “Girl program development and adult learning opportunities” including:

- Salaries and related benefits

- Travel and related expense

- Nonstaff services

- Professional services

- Rent, occupancy and depreciation

- Office, publishing and technology

- Grants and scholarships

- Other expenses

A breakout of these specifics can be found on pg. 7 of the audit.

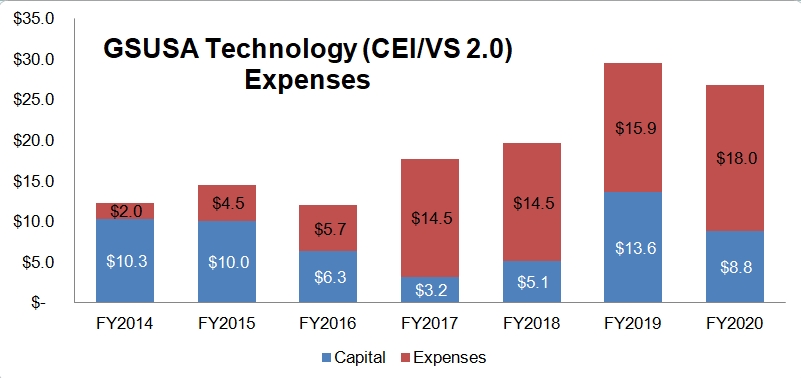

GSUSA is in the process of building and maintaining a council-wide IT platform called Volunteer Systems 2.0 (formally CEI) that all councils are required to use as a part of their charter criteria. Expenses for VS 2.0 cost $26,800,000 ($8.8 mil capital & $18.8 mil expenses) during FY2020 as noted in the 2021 Stewardship Report webinar. Almost $15 million of that was through the use of outside contractors (see Top Contractors table later in this report). Technology costs are included in the “Comprehensive council support” category. Taking out that amount from the council category presents this picture:

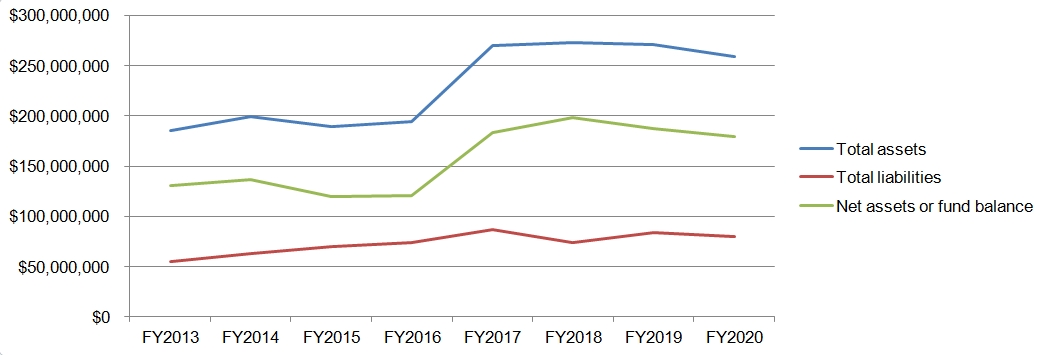

The Consolidated Statements of Financial Position (listing of assets & liabilities) is found on pg. 5 of the audit.

NOTES OF INTEREST

* GSUSA received $9.3 million in a Payroll Protection Program (PPP) loan from the federal government in FY2020 (FY2020 audit, pg. 34). As of the publication of the 2021 Stewardship Report (10/2021), $7.3 million has been forgiven.

* $3,371,045 was spent on legal services in FY2020 (FY2020 990, pg. 16).

* GSUSA spent $58,626,000 on total salaries in FY2020 (FY2020 audit, pg. 7).

* The top yearly salaries of GSUSA’s Officers, Directors, Trustees, Key Employees, and Highest Compensated Employees were as follows (from FY2020 990, pgs. 67-68):

The question marks indicate that the information about the date of employment was cut off in the 990 and unable to be ascertained. These amounts are a combination of a base salary, bonus & incentives, retirement & other deferred compensation, and nontaxable benefits. They notate salaries and not necessarily how much the person received during FY2020. Some individuals received compensation packages once they left GSUSA, but these amounts are not reflected in the above figures.

* Total number of GSUSA staff employed during FY2020: 558 (FY2020 990, pg. 3)

* One GS Media (the website CircleAround) brought in $315,726 of revenue for FY2020. GSUSA originally invested $2.75 million to get One GS Media and CircleAround off the ground (launch date 6/2020), but it is not apparent whether this money was allocated from FY2019, FY2020, or both. More money has been allocated to One GS Media since the original investment, but that will be covered in the FY2021 financial summary. In Sept of 2020, GSUSA released a FAQ about One GS Media and CircleAround. A Statement of Financial Position for One GS Media can be found on page 38 of the FY2020 audit.

* GSUSA’s line of credit was used for FY2020. A line of credit is a preset borrowing limit that can be tapped into at any time. The borrower can take money out as needed until the limit is reached, and as money is repaid, it can be borrowed again in the case of an open line of credit. From the FY2020 audit, pg. 25: “On October 14, 2016, the Organization entered into a $10,000,000, 364 day secured revolving credit facility which is secured by certain of the Organization’s investments. Effective July 6, 2020, the credit agreement was amended with a new increased commitment of $20,000,000 and the expiration date of July 6, 2021. The organization borrowed $7,000,000 in fiscal year 2020 and $0 in fiscal year 2019. Interest expense associated with this borrowing totaled approximately $10,000. The organization borrowed $7,000,000 in fiscal year 2020.”

* GSUSA distributed $3.2 million to councils in the form of grants (2021 Stewardship Report, pg. 47). Specific amounts per council can be found in the FY2020 990 starting on pg. 55.

* A total of $14,678,000 was spent on professional services (FY2020 audit, pg. 7). “Professional services” can involve a number of outside consultants such as, but not limited to:

- Temp services

- Media consultants

- Research consultants

- Translation services

- Training consultants

- Marketing consultants

Note though that the professional services category doesn’t include spending on ALL contractors. Some of those amounts could be lumped in with other categories, such as the case with IT development and legal services.

* Top 5 Contractors (FY2020 990, pg. 85-86):

THROUGH THE YEARS

The following figures are from official audits and differ slightly than what is found in the 990s due to accounting differences. Revenue from FY2018 included the $10 raise in membership dues.

These figures of GSUSA’s assets and liabilities through the past 7 years are pulled from 990s:

Here is the total of GSUSA’s spending on the CEI/VS 2.0 IT platform project from its launch in 2014. Progress is ongoing. These figures come from past Stewardship Reports.

To reiterate, this is a very brief snapshot of GSUSA’s financials for FY2020 and doesn’t include any information about investments and holdings. It is recommended that you consult the audit and 990 for more detailed information and specifics.

FY2021’s summary has also been published.